Fixed vs Adjustable Mortgages in New Jersey: How to Choose What Fits

- Matthew Owens

- Jan 22

- 2 min read

Choosing the right mortgage in New Jersey isn’t just about finding the lowest rate—it’s about aligning your loan structure with your timeline, risk tolerance, and long‑term financial goals. One of the most common decisions buyers and homeowners face is whether to choose a Fixed‑Rate Mortgage (FRM) or an Adjustable‑Rate Mortgage (ARM).

This guide breaks down the differences in plain English, explains when each option makes sense, and helps you decide what truly fits your situation.

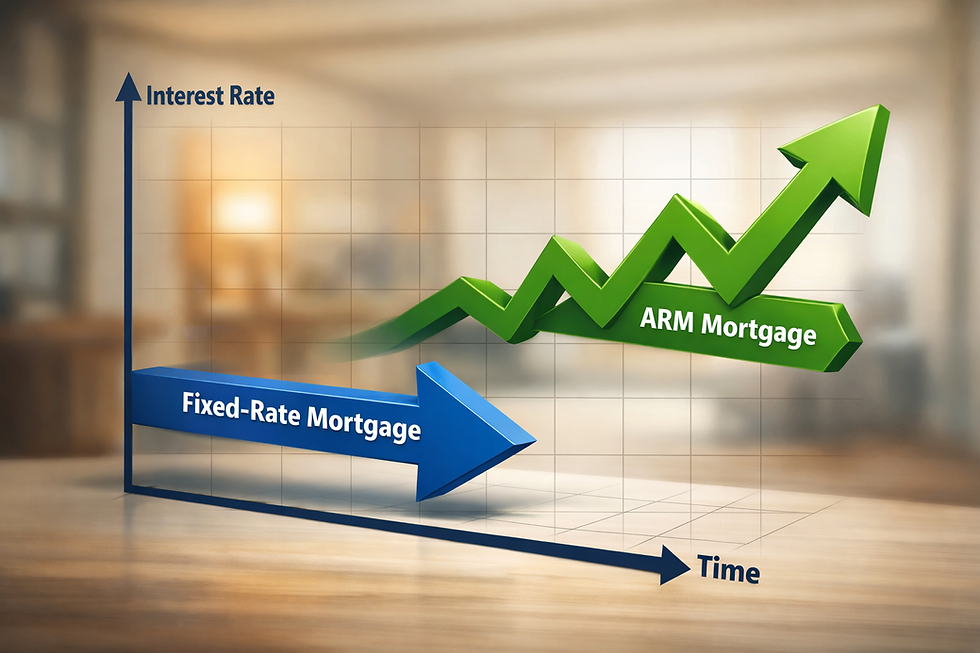

What Is a Fixed‑Rate Mortgage?

A fixed‑rate mortgage has an interest rate that never changes over the life of the loan. Your principal and interest payment stays the same whether rates rise, fall, or swing wildly.

Why New Jersey Buyers Choose Fixed Rates

Predictable monthly payments (ideal for budgeting)

Protection against rising rates

Popular for primary residences and long‑term homeowners

Considerations

Typically starts with a higher rate than an ARM

Less flexibility if you plan to sell or refinance soon

Best for: Buyers planning to stay put long‑term, families prioritizing stability, and homeowners who value certainty over flexibility.

What Is an Adjustable‑Rate Mortgage?

An adjustable‑rate mortgage starts with a lower fixed introductory rate for a set period (commonly 5, 7, or 10 years). After that, the rate adjusts periodically based on the market.

Example: A 5/6 ARM is fixed for 5 years, then adjusts every 6 months.

Why ARMs Can Work Well in New Jersey

Lower initial payments, improving short‑term cash flow

Attractive for high‑income earners, investors, or buyers expecting income growth

Useful if you plan to move, sell, or refinance before the adjustment period

Considerations:

Payments can increase after the fixed period

Requires comfort with some level of rate uncertainty

Best for: Short‑term homeowners, strategic buyers, and those who understand and plan for future adjustments.

Fixed vs Adjustable: Key Differences at a Glance

Feature | Fixed‑Rate Mortgage | Adjustable‑Rate Mortgage |

Interest Rate | Never changes | Changes after intro period |

Monthly Payment | Stable | Can rise or fall |

Initial Rate | Higher | Lower |

Risk Level | Low | Moderate |

Ideal Timeline | Long‑term | Short‑ to mid‑term |

Questions to Ask Before Choosing:

Instead of asking “Which loan is better?”, ask:

How long do I realistically plan to stay in this home?

Would a higher future payment disrupt my lifestyle or savings goals?

Am I comfortable trading stability for short‑term savings?

Is this a primary residence, second home, or investment property?

In New Jersey’s higher‑price markets, the right structure can significantly impact long‑term wealth—not just monthly payments.

A Smarter Way to Decide

The best mortgage isn’t universal. It’s personal.

Two buyers with the same credit score, income, and purchase price may need completely different loan structures based on their goals, timelines, and risk tolerance. This is why transparency and scenario‑planning matter more than headline rates.

A side‑by‑side comparison showing best‑case, worst‑case, and most‑likely outcomes often makes the decision obvious.

Final Thoughts

Fixed‑rate mortgages offer peace of mind. Adjustable‑rate mortgages offer flexibility and opportunity. In New Jersey, where home prices and loan sizes are higher than the national average, choosing the right structure can save—or cost—you tens of thousands over time.

The right answer isn’t about the market. It’s about you.

Comments